In 2026, the question “how much rent can I afford?” is no longer just about picking a number that feels right. With the national rent-to-income ratio hovering near 28-30% and inflation impacting utility costs, using a precise rent affordability calculator logic is essential for financial survival. Landlords are stricter, requiring proof of 40x monthly rent in annual income, while financial planners urge adherence to the 50/30/20 rule.

This guide deconstructs the algorithms behind the best rent calculators. We will move beyond simple guesswork and apply the three industry-standard formulas to your budget: the 30% Rule, the 50/30/20 Rule, and the 40x Rent Rule. Whether you earn $40,000 or $150,000, understanding these metrics is the difference between living comfortably and being “house poor.”

Stop guessing. Use our free Rent Calculator to see your exact safe rent limit based on income and budgeting rules.

The 3 Golden Rules of Rent Affordability

When you use a “how much rent can I afford calculator,” it typically runs on one of these three logic models. Understanding which one applies to your situation is critical.

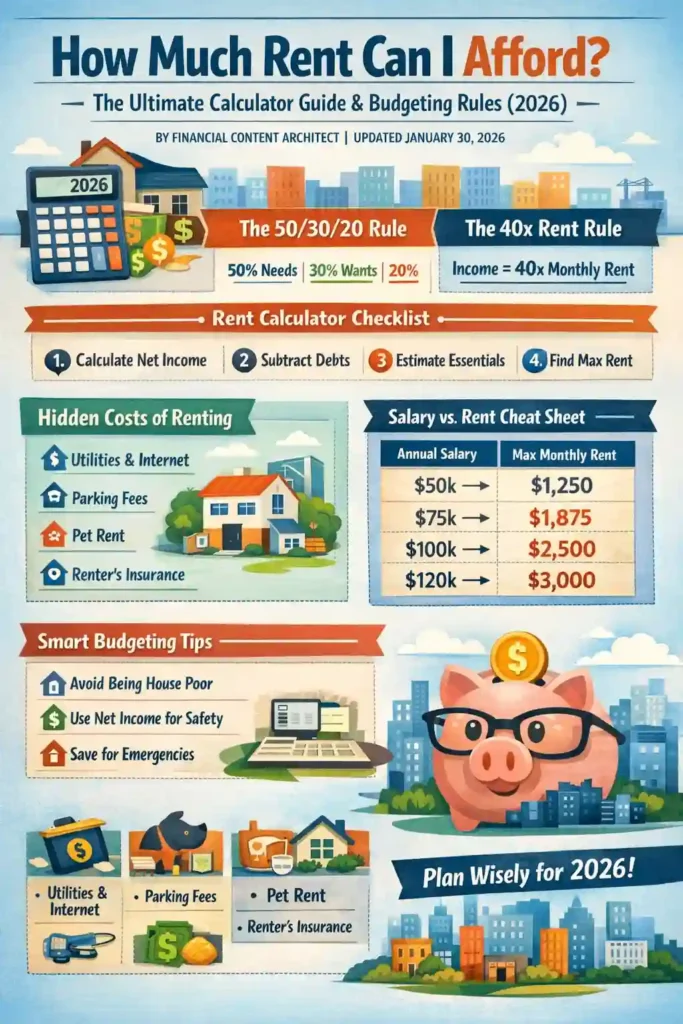

1. The 30% Gross Income Rule (The Industry Standard)

Best for: Quick estimates and standard lease applications.

The Department of Housing and Urban Development (HUD) defines a household as “cost-burdened” if they spend more than 30% of their income on housing. This is the benchmark most landlords and banks use. It is calculated based on your Gross Income (income before taxes).

The Formula:

Annual Gross Income ÷ 40 = Max Monthly Rent

OR

Monthly Gross Income × 0.30 = Max Monthly Rent

Example: If you earn $60,000 per year:

$60,000 ÷ 40 = $1,500/month.

2. The 50/30/20 Rule (The Budget-First Approach)

Best for: People with high student debt, aggressive savings goals, or variable income.

Popularized by Senator Elizabeth Warren, this rule uses your Net Income (take-home pay). It forces you to look at rent as part of your total “Needs” bucket, which must not exceed 50% of your paycheck. This is safer than the 30% gross rule because it accounts for taxes and other essential bills.

- 50% Needs: Rent, utilities, groceries, insurance, minimum debt payments.

- 30% Wants: Dining out, hobbies, subscriptions.

- 20% Savings: Retirement, emergency fund, extra debt payoff.

The Calculation Logic:

1. Calculate Monthly Net Income.

2. Multiply by 0.50 (Total Budget for Needs).

3. Subtract non-rent needs (Groceries, Utilities, Car Payment).

4. Result = Max Rent You Can Afford.

3. The 40x Rent Rule (The Landlord’s Test)

Best for: Competitive markets like NYC, San Francisco, and Boston.

This is not a budgeting tip for you; it is a risk assessment tool for landlords. To qualify for an apartment, your annual gross salary must be at least 40 times the monthly rent. If you fall short, you will likely need a guarantor who earns 80x the rent.

The Reality Check: Even if you feel you can afford $2,500 rent on a $80,000 salary, a landlord applying the 40x rule might reject you because $2,500 x 40 = $100,000 required income.

Manual Rent Calculator: Step-by-Step Guide

Don’t rely solely on automated tools. Run the numbers manually to see where your money is going. Follow this algorithm:

Step 1: Determine Your True Net Income

Check your last 3 paystubs. Average your take-home pay. Do not use your offer letter salary; taxes, 401k contributions, and health insurance deductions can reduce your spending power by 25-35%.

Step 2: Subtract Fixed “Non-Housing” Debts

Before paying rent, you must pay your contractual obligations. Subtract these from your monthly net income:

- Student Loan Minimums

- Car Payments & Insurance

- Credit Card Minimums

- Medical Payment Plans

Step 3: Estimate Variable Essentials

Subtract realistic estimates for:

- Groceries ($300 – $600/month)

- Transportation/Gas ($100 – $300/month)

- Phone & Internet ($100/month)

Step 4: The Remaining Balance

The number left is the absolute maximum you can spend on rent + utilities + savings. To be safe, leave a $200 buffer.

Hidden Costs: The “Plus-Plus” of Renting

Most “how much rent can I afford calculators” fail because they only look at the base rent. In 2026, ancillary fees can add $200 to $600 to your monthly housing costs. You must subtract these from your max rent budget.

| Expense Category | Estimated Cost (2026) | Frequency |

|---|---|---|

| Utilities (Electric, Gas, Water) | $100 – $300 | Monthly |

| Internet & Cable | $60 – $120 | Monthly |

| Parking Fees | $50 – $250 | Monthly |

| Pet Rent | $25 – $75 (per pet) | Monthly |

| Renters Insurance | $15 – $30 | Monthly |

| Move-in Fees (Admin/App) | $200 – $500 | One-time |

| Security Deposit | 1-2 Months’ Rent | Upfront |

Cheat Sheet: Salary to Max Rent Table

Use this quick reference based on the strict 30% Gross Income Rule. If you have significant debt, move one row up (cheaper) to be safe.

| Annual Salary | Max Monthly Rent (30%) | Ideal Rent (25% – Safer) |

|---|---|---|

| $40,000 | $1,000 | $833 |

| $50,000 | $1,250 | $1,041 |

| $60,000 | $1,500 | $1,250 |

| $75,000 | $1,875 | $1,562 |

| $90,000 | $2,250 | $1,875 |

| $100,000 | $2,500 | $2,083 |

| $120,000 | $3,000 | $2,500 |

| $150,000 | $3,750 | $3,125 |

Frequently Asked Questions

Does the 30% rule include utilities?

Ideally, yes. The most conservative interpretation of the 30% rule is that your total housing cost (Rent + Utilities + Insurance) should not exceed 30% of your gross income. If you spend 30% on rent alone, high utility bills could easily push you into the “cost-burdened” zone (35%+).

How can I get approved if I don’t meet the 40x rent rule?

If your income is below the 40x requirement, you have three primary options:

1) Find a Guarantor: A parent or guardian who earns 80x the monthly rent and signs the lease with you.

2) Use a Guarantor Service: Companies like TheGuarantors or Insurent charge a fee (usually 70-110% of one month’s rent) to act as your corporate guarantor.

3) Offer Higher Deposit: In some states (check local laws), offering 3 to 6 months of rent upfront can bypass income requirements.

Should I calculate rent based on Gross or Net income?

Landlords use Gross Income to qualify you. However, for your personal financial safety, you should budget based on Net Income. Using the 50/30/20 rule on your net income ensures you don’t commit to a lease that looks affordable on paper but leaves you cash-poor after taxes and benefits are deducted.

The “Sleep Well at Night” Number

While calculators give you a maximum limit, the smartest rental decision is rarely the maximum one. In 2026, financial flexibility is more valuable than square footage. Aim to keep your housing costs closer to 25% of your gross income if possible. This buffer protects you against rent hikes, inflation, and unexpected life events. Use the calculator logic above not just to see what you can pay, but to decide what you should pay.

{kind=link}